/smstreet/media/agency_attachments/3LWGA69AjH55EG7xRGSA.png)

Follow Us

Follow Us/smstreet/media/media_files/2024/12/05/tdmVL0mw4F6hv2FwbUJH.jpg)

Mr. Gaurav Arora, Fund Manager, Equirus

Historical data suggests that among all asset classes, equities hold the highest potential for long term wealth creation. They are also the only asset class with which one can beat inflation and generate significant long term real returns. However, how one approaches equities is also something that needs an investor’s evaluation. It’s an oft repeated saying that small caps are a faster and better way to create wealth over a period of time and it’s almost fashionable to have one’s entire allocation towards small caps especially these days. But as demonstrated below, reality is more nuanced that that.

First, we look at the hard data and compare returns between multicap index and smallcap index over a long period of time – from 1st April 2005 to 4th November 2024. Over almost 20 years, the Nifty Multicap (50:25:25) total return index (i.e. price returns plus dividends) has delivered an annualized return of 16.6%. Against that, the Nifty Smallcap 250 total return index has delivered 17.1% and the Nifty Smallcap 100 total return index has delivered 15.1% returns.. While some companies within each index would have delivered immense long-term returns, as we can see, chances are that a basket of stocks built using a multicap approach would have delivered equivalent returns to those built solely of smallcap stocks. Consider the fact that there is an element of higher valuation rerating in the small cap space vs large caps (lower starting valuations and higher end-period valuations) and the returns in the multicap space come out better from a volatility-adjusted basis.

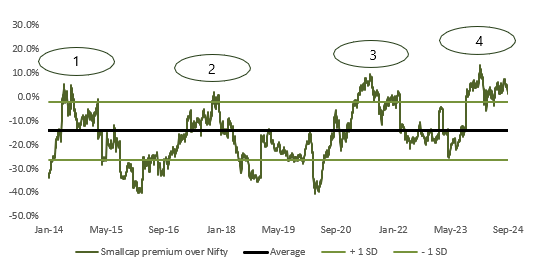

Small caps have indeed had extended periods of outperformance but that is often followed by extended periods of underperformance as well. As can be seen from the chart below of the relative premium of small cap index valuations (as measured by 1-year forward price-to-earnings ratio) over that of the large cap index, there are times when small caps reach very high relative valuations after a period of very strong returns only to underperform significantly over some period thereafter. We have seen 4 such periods over the last 10 years: late-2014, early-2018, mid-2021 and early-2024. The 1-year and 2-year returns of the Nifty and the NSE Smallcap were as follows from those points:

Source: Bloomberg

1-Year return from date | 2-Year return from date | |||

Nifty | NSE Smallcap | Nifty | NSE Smallcap | |

31-Dec-14 | 10.0% | -1.2% | 8.9% | 7.9% |

09-Jan-18 | 4.6% | -29.4% | 16.7% | -36.0% |

19-Jul-21 | 8.9% | -12.8% | 25.9% | 9.1% |

As can be seen, it would have been prudent to reduce exposure to small caps during periods when the valuation premium of small cap index became positive vs the large cap index.

Now that we’ve seen that there are periods when certain segments of the market are more attractive to invest in than others, building a multi cap portfolio is a good way to participate in the equity market opportunity. It allows an investor to benefit by having almost similar levels of returns as well as avoid overexposure to a single segment of the market at inopportune times. A multi cap portfolio gives equivalent returns with lesser volatility and lower chances of extended periods of underperformance and negative returns. If one thinks about it, it is something which is to be expected:

Large companies are often more stable and leaders in their industries with proven long term track records. They can withstand a negative economic cycle much better than smaller companies – they have better access to cheaper capital if required, they can attract better quality talent and pay better, usually have better access to inorganic opportunities, likely to have better competitive advantages given their survival and growth over long periods of time and so on.

Mid cap companies present a balance between risk and return. They often grow faster but are also expected to have higher rates of failure or falter.

Small companies are usually in high growth phase and can be much more nimble and agile; hence they can keep growing much faster than their industries or the economy. However, they also carry the highest risks not only from business, operational and financial perspectives but also their investors typically face higher chances of corporate misgovernance.

Given the relative positioning of these, a blend of investments across market cap curve, depending on individual company’s attractiveness from the perspectives of profitability, growth, competitive positioning, management quality and valuation, is likely to be the best way to invest in an optimum risk-reward manner.

Author: Mr. Gaurav Arora, Fund Manager, Equirus